Public Finance Data and Analysis

Free and Open Access to

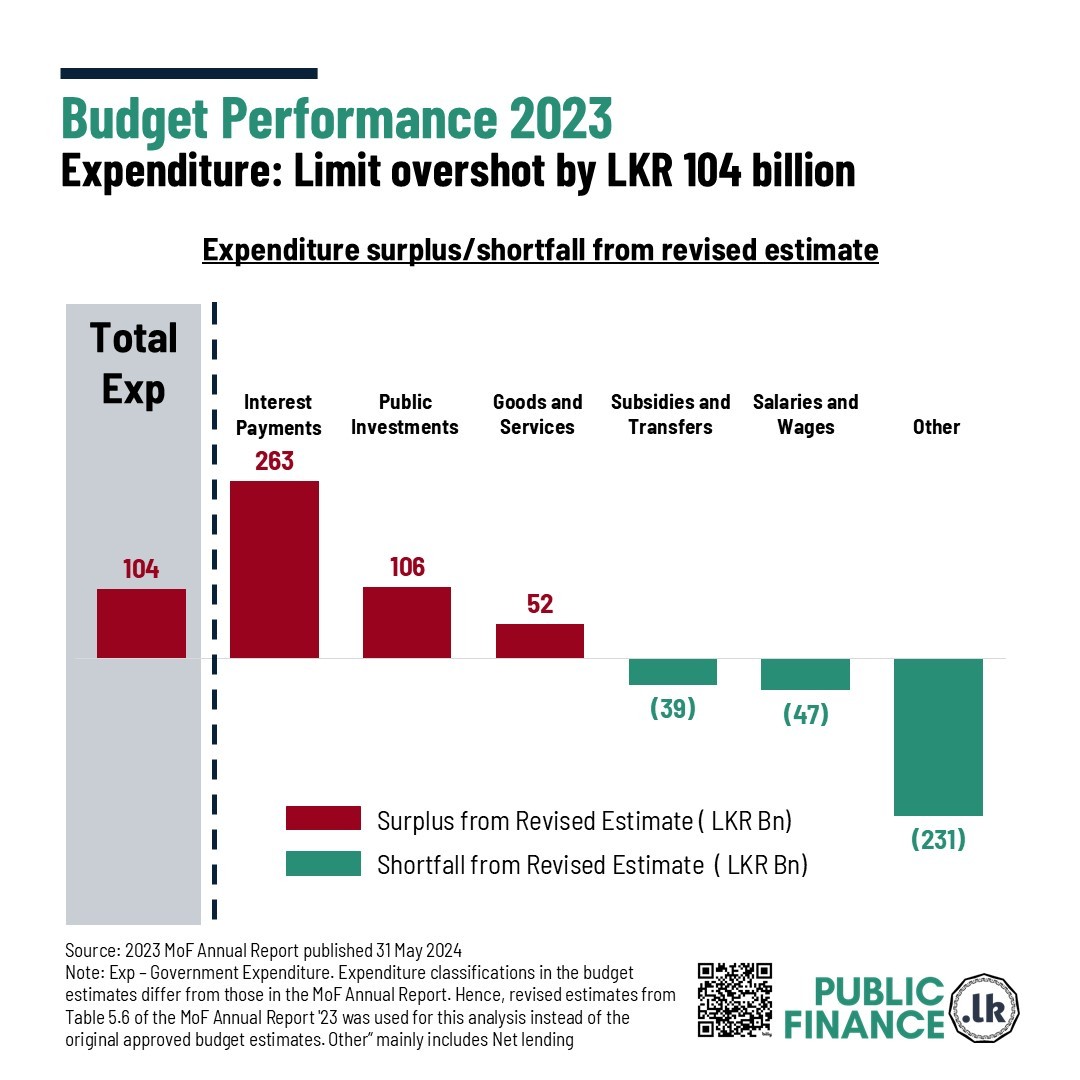

The Ministry of Finance Annual Report, released on 31st May 2024, shows that in 2023, the Government of Sri Lanka exceeded its total expenditure by LKR 104 billion. The total expenditure budgeted based on the government’s revised estimate in 2023 was LKR 5,253 Bn. However, the government spent LKR 5,357 Bn in 2023, which is 2% above the budgeted figure.

This overspending was primarily driven by increased expenditure on interest payments amounting to LKR 263 billion, 12% above the revised estimate for 2023. Public investments increased by LKR 106 billion, and spending on goods and services rose by LKR 52 billion. Conversely, subsidies and transfers decreased by LKR 39 billion, and salaries and wages fell by LKR 47 billion.

Exhibit 1: Comparison of Revised Estimate and Actual expenditure for the year 2023

|

Expenditure |

2023 Revised Estimate |

2023 Actual Expenditure

|

Deviation (LKR Bn) |

Deviation (%) |

|

Recurrent Expenditure |

4,471 |

4,700 |

229 |

5% |

|

Salaries and Wages |

986 |

940 |

(47) |

-5% |

|

Goods and Services |

248 |

300 |

52 |

21% |

|

Interest payments |

2,193 |

2,456 |

263 |

12% |

|

Subsidies and Transfers |

1,044 |

1,005 |

(39) |

-4% |

|

Capital Expenditure and Net Lending |

782 |

657 |

(125) |

-16% |

|

Public Investments |

827 |

933 |

106 |

13% |

|

Other |

(45) |

(276) |

(231) |

513% |

|

Total Expenditure |

5,253 |

5,357 |

104 |

2% |

Note: Exp – Government Expenditure. Expenditure classifications in the budget estimates differ from those in the MoF Annual Report. Hence, revised estimates from Table 5.6 of the MoF Annual Report '23 was used for this analysis instead of the original approved budget estimates. Other” mainly includes Net lending

Source

Ministry of Finance FINAL BUDGET POSITION REPORT (ANNUAL REPORT) 2023 at https://www.treasury.gov.lk/api/file/ad12f7fa-d2db-43d4-9daa-9270ee7b7cac [last accessed 8 August 2024].